From 7 May 2024, The North East Evidence Hub is a project of the North East Combined Authority. Find out more at northeast-ca.gov.uk/north-east-lep

Digital Technology Evidence Base

This evidence base covers an analysis of regional and sector data related to digital technology, a review of the existing literature and an insight into how the digital technology sector links to national policy. It also explores the regional assets that the North East LEP currently has available.

Evidence suggests that the North East digital tech sector has strong potential for growth due to our regional assets and capabilities, which is why it is identified as an area of strategic importance in our North East Strategic Economic Plan.

We have developed an evidence base that looks in detail at the region's digital tech sector, using a range of public and subscription data sources and by reviewing relevant literature.

It provides a snapshot of the current position of the digital tech sector in the North East LEP area and opportunities for further growth in the region. The evidence base was produced over 2022 and is up to date at December 2022. It will be updated again on an annual basis.

The evidence base highlights that the North East has strong foundations in some key subsectors within digital tech in growing parts of the digital market. It also highlights that the sector plays an important role in enabling growth in other sectors. You can read more about the insights from the evidence base in our blog from North East LEP Analyst Thomas Athey here.

Regional Data Analysis

Gross Value Added and Productivity

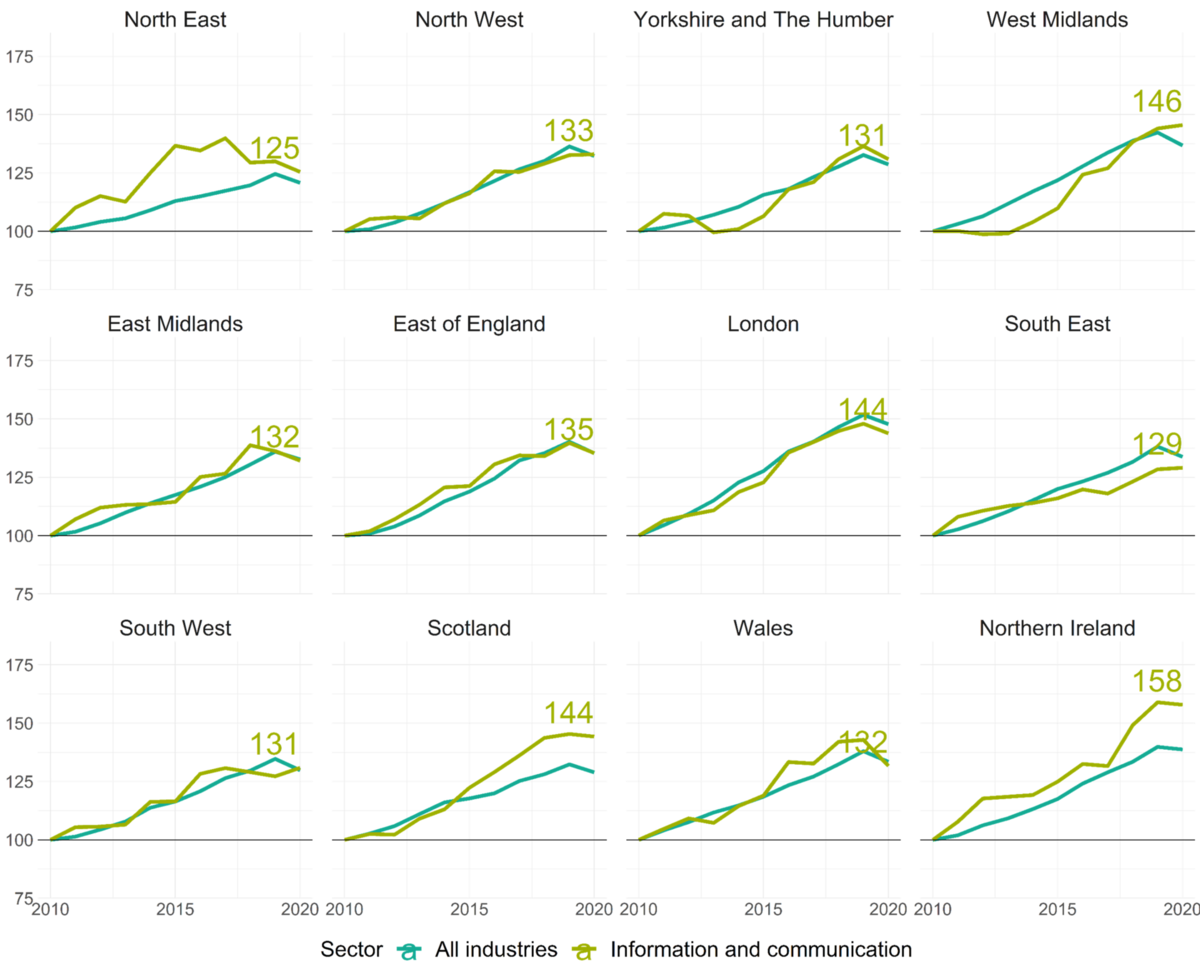

The digital sector grew more quickly than the overall economy in most regions of the UK between 2010 and 2020. In the North East region, the digital sector grew 25% between 2010 and 2020 while the GVA for all industries grew by 21%, highlighting the sector’s potential to contribute to regional economic growth.

This same data suggests that the digital sector in the North East region has been growing more slowly than the sector elsewhere. The 25% growth over the period between 2010 and 2020 is the lowest of all the regions and nations in the UK, 6% slower than Yorkshire and the Humber and 8% slower than the North West. This slower growth is partially due to the sectoral composition of the digital sector in the North East region, with the North East having a high proportion of its digital GVA accounted for by the Telecommunications subsector (59% in 2010). Telecommunications has been growing more slowly than computer programming and consultancy over the last decade limiting the overall growth rate for the North East.

The computer programming subsector is responsible for a much smaller share of the North East region’s GVA. In addition, not only is this subsector smaller in the North East region, but it has also been growing relatively slowly compared to the other Northern regions too.

The digital sector makes a significant contribution to productivity in the North East region, as GVA per hour worked in the sector was £11 higher in 2019 than the contribution of all industries in the North East. Furthermore, productivity in the sector was broadly comparable to other Northern regions, about the same as the North West and higher than in Yorkshire and the Humber. Only London, the South East and the West Midlands had sector productivity significantly higher than the North East.

The trend since 2010 in the sector is more concerning. Productivity in the North East region digital sector peaked in 2016 at £50 but had fell back to £42 by 2019. Over the same period the South East and the West Midlands saw significant growth. Note this is the direct productivity of the sector and does not include the indirect effects of the adoption of digital technologies on wider productivity.

In 2022 there were 2,515 enterprises in the digital sector across the North East LEP. This was 165 less than in 2021, however, this decline was driven by a fall in the number of micro enterprises (with between 0-9 employees). The number of enterprises with 10+ employees increased by 5 over the same period. Of the total enterprises in the sector 615 were in Newcastle upon Tyne, 445 were in County Durham and 390 were in Northumberland.

In 2021 there were 27,000 individuals in employment in digital tech across the North East LEP. 9,000 of these were employed in Newcastle upon Tyne, which had by far the largest number of employments.

Employment in digital increased by 4% between 2020 and 2021. Prior to the Covid-19 pandemic in 2019 there were 30,000 in employment in the North East LEP digital sector.

Employees in the digital sector are much more likely to work from home than average. In 2020 more than half of those working in information and communication worked from home at least some of the time, the highest proportion of any sector.

Total digital enterprises in the North East LEP (2015 - 2022)

Data information: Data is for the North East LEP area. Enterprises are defined as the smallest combination of legal units (generally based on VAT and/or PAYE records) that has a certain degree of autonomy within an enterprise group. Enterprises in the digital area have been defined using 5 digit SIC codes selected by the North East LEP.

Data information: Data is for the North East LEP area by each of seven Local Authorities within the LEP's boundaries. Enterprises are defined as the smallest combination of legal units (generally based on VAT and/or PAYE records) that has a certain degree of autonomy within an enterprise group. Enterprises in the digital area have been defined using 5 digit SIC codes selected by the North East LEP.

Data information: Data is for the North East LEP area by each of seven Local Authorities within the LEP's boundaries. Employments includes employees plus the number of working owners. The BRES therefore includes self-employed workers as long as they are registered for VAT or Pay-As-You-Earn (PAYE) schemes. Self employed people not registered for these, along with HM Forces and Government Supported trainees, are excluded. Employments in the digital area have been defined using 5 digit SIC codes selected by the North East LEP. Subsector totals may not sum correctly due to rounding.

Data information: Data is for the North East LEP area. Employments includes employees plus the number of working owners. The BRES therefore includes self-employed workers as long as they are registered for VAT or Pay-As-You-Earn (PAYE) schemes. Self employed people not registered for these, along with HM Forces and Government Supported trainees, are excluded. Employments in the digital area have been defined using 5 digit SIC codes selected by the North East LEP. Subsector totals may not sum correctly due to rounding.

Data information: Data is for the North East LEP area. Employments includes employees plus the number of working owners. The BRES therefore includes self-employed workers as long as they are registered for VAT or Pay-As-You-Earn (PAYE) schemes. Self employed people not registered for these, along with HM Forces and Government Supported trainees, are excluded. Employments in the digital area have been defined using 5 digit SIC codes selected by the North East LEP.

Data information: Based on responses to three questions in the ONS Annual Population Survey:

1. In your main job, do you work mainly in your own home or in the same grounds or buildings as your home or in different places using home as a base or somewhere quite separate from home? (Respondents were asked where they would usually work in their main job prior to the Covid-19 pandemic).

2. In your main job, have you spent at least one full day in the seven days prior to this interview working in your own home?

3. Do you ever do any paid or unpaid work at home for your main job?

As discussed above individuals may be employed in a digital tech role even if they are not employed by an organisation within the digital sector. There were 47,600 individuals employed in digital occupations in the North East region according to the DCMS definition in 2021. The North East region’s share of employment in digital occupations was the lowest of all the regions of England at 4.1% compared to 5.7% in England excluding London.

The overall role profile in the North East was relatively similar to elsewhere, but there are a few occupations where the North East shows significant variation compared to other regions. For example, the North East has significantly more IT user support technicians, 16% of the digital workforce was employed in this occupation compared to just 7% of those in England excluding London. In contrast the North East has many fewer IT business analysts, architects and systems designers (5% in the North East compared to 13% in England excluding London).

Positively, the total number of digital occupations was 47% higher in 2021 than 2015 in the North East, compared to 39% higher in England excluding London. The biggest increases during this period were in the number of programmers and software development professionals (105%), IT user support technicians (85%) and IT specialist mangers (80%).

In terms of how digital occupations are segmented by sector there is some data available from the three-year pooled annual population survey. This data is limited as only two digital occupations are available, and the sector classifications have been pooled into different categories. Nevertheless, this data highlights that only 39% of those employed in digital occupations between 2019 and 2021 were employed in the digital sector itself (information and communication). The next largest employers of digital occupations in the North East were public administration and defence, financial and insurance activities and Education. This emphasises the importance of digital tech in enabling growth in other sectors.

Proportion of digital employment by occupation and region (2021)

Demand for digital tech workers in the North East LEP area is very high. Over the 12 months between July 2021 and June 2022 there were more job postings for IT jobs than any other occupation category. In addition, software developer was the 6th most common occupation amongst job adverts over the same period (4,547 postings). Given that digital occupations account for a relatively small proportion of total employment in the North East LEP this strongly suggests that there is a skills shortage in relation to these occupations.

There is greater demand for IT jobs than roles in the digital sector itself, with there being 4,001 postings in the sector over the same period. This was only the 5th highest number amongst high-level sectors, which implies many of those recruiting for IT positions are doing so outside of the digital sector. Within the IT sector, the most in demand occupations were software developers and consultants, both with almost 200 postings. However, there was clear demand for other supporting occupations too. Only around 48% of the jobs advertised were IT jobs, with the next largest high-level groupings being Engineering Jobs, Sales Jobs and Creative & Design Jobs.

The North East LEP area benefits from four universities, Durham, Newcastle, Northumbria and Sunderland, providing higher education qualifications and skills to students in the region. In 2020/21 there were 5,165 students enrolled in computing degrees in these four universities, the second highest number of computing students in the core cities after Manchester. A further 1,855 were enrolled in mathematical sciences and 3,950 enrolled in physical sciences. The North East LEP contains a slightly lower share to the national total of students studying computing degrees than its share of the total number of students in higher education (3.5% versus 3.7%).

In terms of the specific computing related subjects studied in the North East LEP area, compared to nationally the North East LEP has a greater proportion of its computing students enrolled in computer science and software engineering. On the other hand, the North East LEP has a small percentage of students enrolled in Computer games and Animation and Artificial intelligence degrees.

A relatively small proportion of those completing apprenticeships in the North East LEP do so in the information and communication subsector. In 2020/21 only 2.9% did so in the North East LEP, compared to 4.8% in England.

Number of job adverts posted by occupation category in the North East LEP area (July 2021 - June 2022)

The digital sector has the highest median gross weekly pay of all sectors in the North East region, with the median gross weekly wage of £604 considerably above the median for the North East region across all sectors (£458). This further highlights the quality of the jobs and why growth in the sector is so valuable for improving regional employment prospects.

The pay gap between the North East and the UK in the digital sector is significant, the second largest after the gap in financial and insurance activities. This can cause problems for North East firms who may struggle to attract and retain talent. This particularly true as working from home is increasingly prevalent in the sector due to the impact of Covid-19, which may allow high paying firms in the rest of the UK to recruit from further afield.

Digital sector roles are generally well renumerated. All but one of the digital sector roles (for which there is available data) have median gross weekly wages clearly above the North East Median wage. As was highlighted in the occupations analysis above however, the North East region has a lower share of regional employment in digital occupations. In addition, an above average share of its regional employment is in IT user support technicians, which have a median wage close to the North East median. The broader growth of digital occupations in the North East may not contribute to increasing the median income in the North East as effectively as it might elsewhere because of these limitations.

Similar to the digital sector overall, most digital sector roles are not as well renumerated in the North East as they are nationally. The largest differences are for IT specialist mangers and programmers and software development professionals. In contrast, information technology and telecommunications professionals, are nearly as well renumerated in the North East as nationally. This may be linked to the relative size of the telecommunications sector in the region, as discussed in the GVA section.

Median gross weekly wage by sector, North East and UK (2021)

Digital infrastructure in the North East LEP area is generally of a high standard, but there are challenges with access in the more rural areas of the North East LEP. Over 94% of premises in every local authority in the North East LEP have access to superfast broadband (97% of premises in the median English local authority have the same level of access). Access to ultra-fast broadband, full-fibre and gigabit is also very strong in Newcastle and North Tyneside, where most of the digital sector businesses in the North East LEP are located. Northumberland generally has lower access to these faster broadband connections, with only 23% of premisses having access to ultrafast broadband, 21% access to full-fibre and 21% access to Gigabit. Access to full-fibre broadband is also low in Gateshead, South Tyneside and Sunderland, while access to ultrafast and gigabit broadband is low in County Durham.

Investment, research and development expenditure and innovation

Investment is crucial for firms to grow and scale. Data on venture capital investment in the digital sector by region is available from the UK government’s 2021 Tech Nation report. In total there has been £726M invested in the North East digital sector between 2015 and 2020. However, investment in England excluding London has been growing at a quicker rate than in the North East in recent years.

While not directly related to the digital sector, the North East region also receives lower levels of research and development (R&D) expenditure per head than England excluding London. For instance, in 2019 the North East region received £386 per head less than England excluding London. This is significant as research and development spending is one of the key drivers of business innovation and growth. R&D also often requires the use of technology to be effective. Lower levels of investment are likely to act as a constraint on the wider growth of the tech sector.

There is no comprehensive database containing expenditure on research and development in the digital sector but Innovate UK releases data on its grants awarded in the AI and data economy subsector that can serve as a proxy. The North East region’s share of grants awarded is considerably lower than its share of the national workforce and these grants also have tended to be of a smaller size than the grants received by other regions. Similar to R&D spending this is likely to act as a constraint on sector growth.

Innovation is a key driver of regional growth at both a firm and sector level. However, innovation is difficult to measure directly and there is no regional sector data in the ONS innovation releases. The Data City platform, discussed in more detail in the next section, provides a novel means of understanding the number of innovative firms using by searching for key innovation related terms on companies’ websites. The data from this platform suggests that firms registered in the North East operating in the digital sector are much more likely to be highly innovative. 30% of all highly innovative firms are in the digital sector, compared to just 6% of firms in the region overall. This suggests that the digital sector is not only highly innovative itself, but also that it is a source of regional innovation that can enable growth in other sectors.

Source: Gross domestic expenditure on research and development, UK (ONS; last updated 4 Aug 2021) Data information: Expenditure rate is £m per 10,000 adults. Based on UK nations and English regions - the North East region includes the North East and Tees Valley LEP areas. Northern Powerhouse regions are the North East, North West and Yorkshire and the Humber regions. The "greater South East" is made up of three regions: London and the South East and East of England. Adult population is all people age 16 and over (mid-2019 estimates)

Service exports from the digital sector make a modest contribution to overall service exports from the North East region. In 2020 the North East region exported services worth £298 million from this sector, 6% of the regional total. North East exports per individual employed in the sector are lower than the other Northern regions.Service exports from the digital sector make a modest contribution to overall service exports from the North East region. In 2020 the North East region exported services worth £298 million from this sector, 6% of the regional total. North East exports per individual employed in the sector are lower than the other Northern regions.

The North East’s exports from the sector are relatively evenly balanced between EU and non-EU markets. In 2020 44% of the exports were to EU markets compared to 56% to non-EU markets.The North East’s exports from the sector are relatively evenly balanced between EU and non-EU markets. In 2020 44% of the exports were to EU markets compared to 56% to non-EU markets.

Nationally there has been very strong growth in foreign direct investment (FDI) in software and computer services in recent years. In 2021-22[1] 26% of all new jobs created though FDI were in software and computers services. The total number of new jobs created in the sector was 22,400 and the total had grown 104% since 2016-17. While LEP level data is not available by sector, it should also be noted in the same year the DIT inward investment results showed that the North East LEP created the largest number of jobs through FDI of any area outside of London.

The results below are the key findings from the Data City platform relating to nine tech related sectors in the North East LEP. This platform links companies house data to companies’ websites and uses the website text and machine learning to classify firms into Real Time Industrial Classification Codes (further detail can be found in the methodology section).

The methodology is not perfect and the total number of firms may differ to those found in other sources. However, by applying a consistent approach across the UK the platform allows us to compare the sectors in the North East LEP to other regions. The findings in this section focus on the degree of specialisation in the North East LEP area, the extent to which the sector is a branch economy, overlap with other sectors and regional subsector specialisations

Artificial intelligence

49 with locations in the North East LEP

Moderate LQ in North Tyneside

47% of North East LEP firms with out of region locations, 21% nationally

Over 10% of firms in the sector also operate in advanced manufacturing, internet of things, computer hardware, photonics and data landscape

Strong regional specialisation in systems optimisation and a moderate specialisation in green tech, Industry 4.0 and Life Sciences

Cyber

128 firms with locations in the North East LEP

Very strong LQ in Gateshead, strong LQ in North Tyneside, moderate LQs in Newcastle and Sunderland

66% of North East LEP firms with out of region locations, 26% nationally

Over 10% of firms also operate in Data infrastructure, Data landscape and Fintech

Moderate regional specialisations in Network security, threat management, endpoint security and incident detection and response

Digital creative industries

240 firms with locations in the North East LEP

Moderately high LQs in Newcastle, Northumberland and Gateshead

29% of North East LEP firms with out of region locations, 15% nationally

Over 10% of firms in the sector also operate in agency marketing, research and consulting, and business support service

Moderate regional specialisations in photography, advertising, architecture and design

Ed Tech

23 firms with locations in the North East LEP

Moderate LQ in North Tyneside

26% of North East LEP firms with out of region locations, 20% nationally

Over 10% of firms also operate in advanced manufacturing and digital creative industries

Moderate regional specialisations in Digital learning, immersive experiences and learning management systems

Fintech

209 firms with locations in the North East LEP

Very strong LQ in Newcastle and a strong LQ in North Tyneside

75% of firms with out of region locations (25% nationally)

Over 10% of firms also operate in software as a service

Very strong regional specialisation in buy now pay later technology, moderate specialisation in insurtech, professional services and prop tech

Gaming

27 firms with locations in the North East LEP

Moderate LQs in Gateshead, North Tyneside, Newcastle and Sunderland

44% of North East LEP firms with out of region locations, 17% nationally

Over 10% of firms also operate in digital creative industries, immersive Tech, and advanced manufacturing

Moderate regional specialisations in Enabling technology, Game development studies and Publishers

Immersive tech

16 firms with locations in the North East LEP

Very strong LQ in Gateshead, moderate LQs in Newcastle and North Tyneside

25% of North East LEP firms with out of region locations, 19% nationally

Over 10% of firms also operate in digital creative, Ed Tech, gaming, advanced manufacturing, design and modelling tech, and streaming economy

Moderate regional specialisations in AR, VR and Media

Med tech

34 firms with locations in the North East LEP

Moderate LQs in in Durham and Northumberland

68% of North East LEP firms with out of region locations, 23% nationally

Over 10% of firms also operate in advanced manufacturing, electronics manufacturing, advanced materials, photonics, quantum economy, space economy, sensors, clean tech, computer hardware, and automotive vehicles.

Very strong regional specialisation in advanced materials, moderate specialisation in photonics and imaging

Software as a service

76 firms in the sector with locations in the North East

Strong LQ in Newcastle upon Tyne, moderate LQs in Northumberland and North Tyneside

70% of North East LEP firms with an out of region locations, 30% nationally

Over 10 % of firms also operate in Fintech and Data infrastructure

Very strong regional specialisation in real estate, moderately strong specialisation in development and finance and accounting

Conclusions

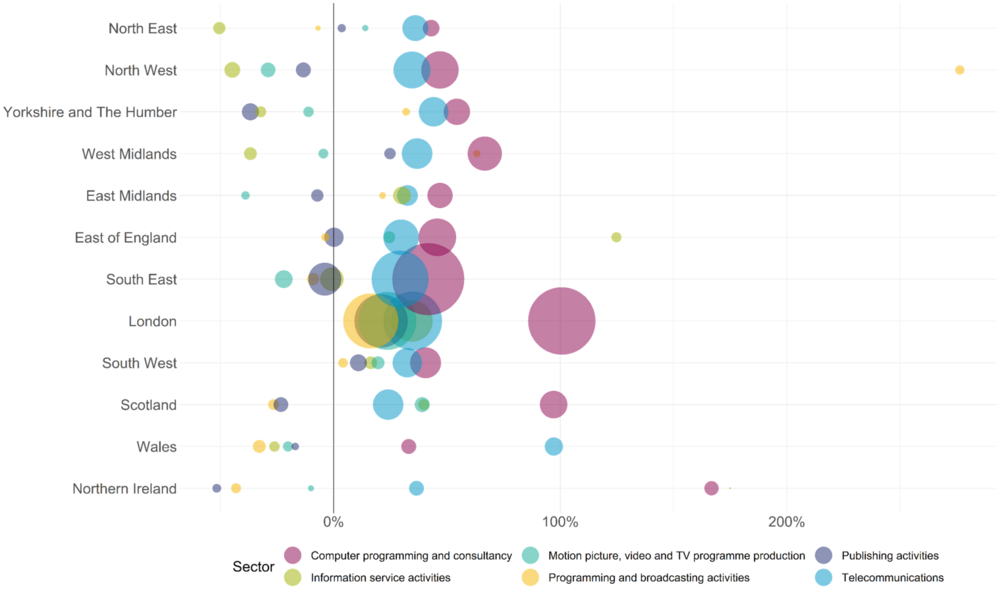

Cyber, fintech, immersive tech and software as a service are the sectors which the North East LEP has at least one strong location quotient, meaning these are the sectors where the North East LEP has a greater concentration of firms than the national average.

For most sectors, a much larger proportion of firms in the North East LEP had out of region locations than the sector nationally. This is likely indicative of a strong branch economy and suggests the sector in the North East is partially dependent on out of region firms. A few sectors however, had a lower proportion of such locations, especially immersive tech, ed tech and digital creative industries.

All sectors had at least some dependency on other sectors. The sectors that demonstrated the strongest degree of crossover were AI, cyber, digital creative, gaming, immersive tech and med tech. This suggests that these sectors have a supporting role in the wider digital ecosystem.

Finally, the North East does not have a specialisation within all these sectors, but it does have a strong regional specialisation within AI, fintech, med tech and software as a service. This may indicate that the North East has a competitive advantage in these fields.

Literature review

Growing sectors

Global trends suggest several technological advancements will be crucial to digital sector development, including artificial intelligence (AI), cybersecurity, virtual reality (VR), robotics and internet of things (IoT). This sections explores which sectors have been highlighted in the existing literature as growth areas for the North East.

Research by Tech Nation shows that the UK is in the top ten countries globally for consumer fintech adoption and investment in the technology doubled between 2018 – 19[1]. The strength of the UK is also echoed in Deloitte’s 2019 Technology Fast 500 winners for Europe, Middle East and Africa, in which the UK had three of the top ten fastest growing companies[2]. These firms were all in the Fintech sector.

The Department for Digital, Culture, Media and Sport’s (DCMS) report into Regional Digital Ecosystems suggests the existence of clusters and industrial specialisms can lead to greater regional growth[3]. The North East already has a proven track record in fintech with success stories such as Sage and Atom bank, two Fintech businesses that have experienced strong growth and expansion. Sage is the ‘world’s third largest supplier of enterprise resource planning software’ according to research by Urban Foresight, while Atom bank is often recognised as a future unicorn. Both companies were recognised by DCMS as an asset to the North East due to the clustering of specialist services provided by these organisations.

However, there is significant strength in depth in the North East fintech cluster too. Research into the North East Fintech Ecosystem by Whitecap Consulting estimates that there are 58 Fintech firms in the North East and approximately 3067 Fintech related roles[4]. Significantly, Whitecap’s research also shows that the North East is the only region in the North with a dedicated Fintech cluster. The networks and knowledge base embedded in the cluster can attract businesses and investment to the region. Indeed, of the Fintech businesses in the North East, a higher percentage are start-ups than in any other region, which suggests that new firms are already choosing to locate in the region to benefit from the existing cluster.

^North East Fintech Ecosystems Report 2019 - 2020, White Cap Consulting, 2019

Artificial Intelligence (AI) is one of the key tech subsectors for the UK, with the Government publishing a National AI Strategy that sets out plans to solidify the UK’s position as a global powerhouse in AI[1]. This strategy grouped together its actions under three pillars, investing and planning for the long term needs of the AI ecosystem, supporting the transition to an AI-enabled economy, and governing AI effectively.

The UK has the third highest level of AI investment in the world and UK digital investment is dominated by AI. While reports show that London is the centre of AI business, there is a small cluster in the North East. Several research networks and organisations are identified by Professor Dame Wendy Hall and Jerome Pesenti in their report Growing the Artificial Intelligence Industry in the UK[2]. The North East is also home to the National Innovation Centre for Data in Newcastle, which is recognised as an asset that can develop AI technology as well as create networks in the region that join industry, academia and the public sector.

Several other tech sectors have been identified by researchers as potential growth areas for both the UK and the North East. Modelling by Steer-Economic Development suggests that the North East digital sector could grow by at least £460 million in annual GVA by 2025, which would create 13,800 additional jobs[1]. They found that the most common sectors amongst high growth digital firms in the region included Software-as-a-Service (25% of firms), mobile apps (21%), analytics, insight, tools (19%) and other software (19%). Areas for future growth potential were also identified in subsea robotics, marketing tech, gaming and immersive tech, and transport tech . There is clear overlap here with research recently commission by the North East LEP looking at key future markets for the region[2]. This research examined a range of future trends and existing regional specialisms and identified 17 markets that present growth opportunities. Several of these related to digital tech including immersive tech, robotics, software development, cloud computing, cybersecurity, payment processing and data analytics (in addition to Fintech).

^Future economic markets forsight report (To be published)

The conditions for growth

Even dynamic sectors such as the North East digital tech cluster need the right conditions to grow. This section explores the conditions required for the digital tech sector to grow in the North East.

With the growth of the digital tech sector globally the demand for skilled employees to fill job vacancies in the sector is increasing at a substantial rate. The DCMS predicts that by 2025 a further 678,000 jobs could be created within the UK digital sector.[1] Other research has also found that between 2020-21 there was a 50% rise in tech job vacancies across the UK and a 53% rise in digital employment since 2010, which is significant when compared to the overall UK employment growth of 12%. The most in demand roles across the country in 2021 were software developers, with programmers, web designers and IT business analysts also in high demand. Whilst this is positive in terms of employment and growth, skills forecasts suggest that there may not be enough skilled workers to fill all these roles. The UK government’s Digital Strategy predicts a loss of £63 billion per year in GDP due to the general digital skills gap, highlighting how significant the issue is.

The growth in digital employment opportunities has certainly occurred in the North East too, but there are reasons to believe that the North East faces particular skills and recruitment challenges. A recent survey fielded by Sunderland Software City (SSC) found only 43% who respondents in the North East were able to recruit to their advertised roles, compared to the national average of 79%. While the digital skills gap may be a national issue, the North East is particularly struggling to develop a strong digital tech workforce. Not only this, but when digital recruitment does occur in the North East workers appear to be less experienced and less likely to work in core digital occupations. SSC found that only 19% of those working in the sector in the North East had over 15 years’ experience, compared to 28% nationally. The DCMS has also found that tech workers in the North East are less likely to work in tech businesses, while SSC reports that many of the roles recruited for by North East IT businesses are focussed on roles in marketing, sales and design.

One of the reasons for the recruitment challenges in the North East is the relative compensation on offer for digital tech workers. With digital tech salaries estimated to be 48% higher than the average salary the sector is very competitive in terms of recruitment. Reports show that the North East is in the bottom quartile for median pay in the digital sector, which makes it harder to attract and retain employees who could potentially earn more by working in a different region. This is issue has likely been reinforced by the rise of remote working due to Covid-19. While the literature does not currently focus on this issue due to its recent development, it is likely a topic that will become more significant as remote working becomes more embedded into working culture across the country. At that point regions such as the North East could face further recruitment issues, as locals are able to live in the region but work for an organisation in London and the South East or even in another country, which offers a more competitive salary. While this may mean that overall, the North East economy is able to benefit from increased wages for its residents, it could hinder the growth of local firms who are unable to compete with their southern counterparts for the highly skilled workers.

In terms of skills generation the North East is home to four universities as well as many further education providers. Furthermore, reports show that the region is home to the highest number of postgraduate computing students per head of population, which should suggest the region is relatively well positioned from a recruitment perspective. However, the North East also has the lowest proportion of working age residents with any degree-level qualification in the UK, due to both low participation in higher education and a low rate of graduate attraction. Graduate retention is cited as a particular issue for the digital tech sector, with several reports into different areas of digital tech, including Fintech and AI, highlighting the lack of talent as a major issue.[2]

Digital exclusion may also be limiting the development of tech related skills in the North East. A Digital Skills Exclusion report published by the North East LEP[3] found that approximately 8% of people in the North East are offline, compared to 5% nationally. They also found that basic Microsoft Office Skills were most in need of improvement, followed by knowledge in specialist software or hardware. The lack of generic digital skills, such as the ability to competently use popular computer programmes, hinders the digital tech sector’s ability to upskill an average worker into the more technical roles needed to fill vacancies.

^Assessing the UK’s Regional Digital Ecosystems, Department for Digital, Culture, Media & Sport, 2021 Assessing the UK’s regional digital ecosystems - GOV.UK (www.gov.uk)

Digital tech is generally recognised as a relatively stable sector that can support economic growth through productivity gains and innovation. For this reason, investment into the sector is highly competitive and sought after. The UK Government’s Digital Strategy[1] outlines investment as one of the country’s key strengths, highlighting that a third of the £89.5 billion invested into European tech was directed to the UK. It also reports that £27.4 billion of private capital was raised in 2021 in the UK, which is double that of second placed Germany. The UK’s position in Europe is therefore strong in terms of digital investment, making the country well-placed to grow competitive and innovative businesses. While London and the South East are still leaders in attracting digital investment to the UK, there is a significant amount of venture capital spread across the country. Approximately £9 billion of the £27.4 billion venture capital invested into the UK in 2021 was spread across regions outside London and the South East.

For the North East this means that there is some interest in projects outside the historically core areas of tech development and an opportunity to attract further investment to the region. However, the Department for Digital, Culture, Media and Sport’s report on Assessing the UK’s Regional Digital Ecosystems[2] did highlight that venture capital can be difficult to access outside London and the South East, due to the high concentration of output in these areas. With cities such as Manchester, Edinburgh, Leeds and Birmingham ranking higher than Newcastle in the Levelling Up Power Tech League 2021, there is a risk that investment is attracted to other regions such as the North West, Scotland and the Midlands. There is therefore a gap between the theoretical opportunities highlighted in the literature and the practical application of this from investors.

^Assessing the UK’s Regional Digital Ecosystems, Department for Digital, Culture, Media & Sport, 2021 Assessing the UK’s regional digital ecosystems - GOV.UK (www.gov.uk)

Research and development expenditure is often cited as a key factor in improving business and regional growth prospects. The UK Government has pledged a £20 billion investment into R&D by 2024 -25, showing the value placed on innovation by the Government. This investment in research and development is essential in maintaining and growing the UK’s digital presence, especially in digital as nearly one fifth of total UK business R&D in 2020 was spent on digital technologies. The Government’s Digital Strategy[1] also specifies the importance of universities and higher education in powering digital innovation and commercialisation. The North East is well placed to benefit from this focus on education and business partnerships given its 4 universities. The literature suggests that regions such as the North East which may struggle to attract private investment would benefit from maximising publicly funded research opportunities and growing partnerships between researchers and tech businesses.

One common theme in the literature around technology growth is the importance of sector networks. A report into Italian competitiveness and innovation[1] for instance suggested that countries such as Italy struggle to innovate and grow at the same level as the UK due to their fragmented business networks which do not allow for shared risk. In contrast the UK is home to a range of networks that help to connect tech organisations and allow them to share risk, investment and costs. An example of this is the nine Catapults across the UK that work to direct investment across the country, of which three have centres in the North East LEP area. This may partially explain why Tech Nation found in their UK Tech for a Changing World publication that the UK is home to 77 tech unicorns, which ranks the UK third globally, behind only the United States and China and far ahead of its European counterparts (Germany was on 56 and France on 31).

The existence of a range of networks and clusters is one of the existing strengths of the North East tech sector. Economic consultancy firm Urban Foresight found that 77% of companies in the North East belong to a digital cluster.[2] The region is also home to several national innovation centres, four universities, and digital accelerators, which further strengthens the ability of businesses to innovate while sharing the risk and costs with local partners.

^Competitiveness and Innovation in High-tech companies: an application to the Italian Biotech and Aerospace industries, Armando Calabrese et al., https://journals.sagepub.com/doi/pdf/10.5772/56755

The UK government is attempting to grow the digital sector through several interventions, such as increased public investment and skills programmes. These interventions are intended to improve tech data, strengthen digital infrastructure, make the regulatory framework more accessible and ensure the security of the digital environment. An example of this is the continued funding of the United Kingdom Research and Innovation (UKRI) body, which aims to drive investment in research and development and therefore strengthen innovation. Tax reliefs for research and development investment have also been implemented and expanded to include cloud computing and data acquisition. The available literature suggests that these government policies do have a significant positive effect, however it should be noted that knowledge of these policies is key to their success and without informed networks in place to support organisations and share information the interventions may not be as effective as possible.

Research also suggests that existing clusters and business support are amongst the conditions required for businesses to flourish. A report into the Twelve Clusters of Tech in the North East[1] identified a strong infrastructure in place in the region including the digital accelerators, tech workplaces, PROTO in Gateshead and innovation centres. As well as regional support, established sectors such as AI and FinTech will be essential to ensuring investment is attracted to the North East tech sector. Established businesses improve the regional facilities and infrastructure through investment as they grow, which can then attract start-ups to the area. Therefore, the knock-on effect of having a few very successful digital tech sectors in the region, such as Fintech and AI, is the potential growth of other sectors, such as Data Analytics, who can take advantage of the regional facilities and infrastructure developed by others.

Growth in the North East's tech sector can also lead to growth in the wider economy through digital transformation. This section explores how technology can enable growth in other areas.

With the economic shocks that followed the Covid-19 many sectors faced struggles to grow and, in some cases, survive. However, the digital tech sector was well-placed to provide the innovative solutions needed to adapt to these changes. Many companies in the sector quickly changed their models to meet the needs of their customers, while organisations that did not previously have experience in digital tech began to transition into the space. Starbucks is presented by Accenture in their 2021 Tech Vision report[1] as a global example of digital transformation, with the development of their mobile app being a key lifeline for the company during the pandemic. The pandemic also accelerated a move to cloud-based working with organisations such as the NHS moving to Microsoft Teams to allow for effective remote working. These swift digital transformations have allowed firms in the digital tech sector to solidify their position as essential services in the modern era. Many organisations in the sector have also been able to accelerate innovation by providing solutions to problems posed by the pandemic, such as online systems that allow for remote health visits. This innovation was supported by Government grants issued to small businesses to support in their Covid recovery by allowing the organisations to invest into solutions that would help build their resilience against future shocks or take advantage of opportunities to innovate and scale up.

The UK’s transition out of the EU has provided some opportunities for the digital tech sector with a need for innovative solutions to facilitate cross-border working. For example, the need for smart border technology in areas such as Northern Ireland is a digital challenge that several tech companies are currently working on.[1] EU exit has also created opportunities for new global partnerships. The UK’s Digital Strategy outlines a number of partnerships that have been made possible including a UK-US Tech partnerships, strengthened tech relations between the UK and India and the UK, and closer links to the Association of South-East Asian Nations (ASEAN) Digital Innovation Partnership.

However, while the digital tech sector may have some new opportunities arising out of EU exit, they are constrained by an uncertain regulatory environment brought about by changes to policies. For example, the changing immigration system may make it more difficult to attract workers from the EU,[2] while issues around trade policies may mean UK firms struggle to trade with the EU as effectively. One issue highlighted by North East businesses specifically are the challenges around employing workers on short-term visas for limited-time projects. The UK digital strategy appendix[3] highlights the visa journey for digital tech employers, with six potential visas available, as well as guidance around how to sponsor licence. The information, however, can be quite overwhelming and time-consuming for employers to understand. These issues could hinder growth as firms focus on understanding the regulatory changes instead of innovating and developing their products.

The potential productivity gains for the wider economy resulting from a strong digital tech sector are significant, with tech developments able to transform the way we currently work in the UK. For instance, a 2015 report into the effects of Chinese high-tech industry on the national economy illustrated the impact of the tech sector on secondary industries such as agriculture.[1] The report found that the tech sector can lead the transformation of more traditional sectors, enabling them to increase productivity through innovation and automation. An investigation into the importance of high-tech companies for EU economies[2] also highlighted the benefits of innovation in improving efficiency and increasing productivity across sectors. Within the UK, Artificial Intelligence specifically is predicted to have a large impact on productivity as it can provide companies with the ability to optimise their planning and use their resources efficiently. Professor Dame Wendy Hall and Jerome Pesenti’s report into Artificial Intelligence[3] suggests that the technology could increase productive capacity by 20% through machine learning leading to higher efficiency. They illustrate the importance of this to companies by highlighting that 78% of firms believe AI will improve efficiency and 49% believe it will transform their industry. For the UK the paper predicts a 10.3% increase in UK GDP because of AI adoption.

^The importance of high-tech companies for EU economy – Overview and the EU grand strategies perspective, Alenka Pandiloska Jurak, DOI: 10.2478/rsc-2020-0013

While the literature is clear on the positive effects of the digital tech sector on traditional industries, consideration must also be given to how the sector will develop through interactions with industries such as offshore wind or electric vehicles. The opportunities provided by merging digital tech with other developing industries are predicted to transform the way businesses currently work by producing innovative solutions in response to new problems.[1] Technology such as Internet of Things, Cloud Computing and AI are being built to allow other industries to develop smart factories that collect real time data from various sections of a business such as HR, the factory floor, or sales to make decisions that optimise the companies’ resources.[2] This data driven planning is intended to allow companies to react efficiently to changes in their processes.[3] A timely example of this is a clean energy supplier using technology to monitor the increased demand for offshore wind energy due to the Russian invasion of Ukraine, while also monitoring the number of absences due to Covid and then calculating how this will impact their ability to satisfy increased demand with a reduced workforce. The literature suggests that by adapting to a technologically advanced, data driven approach many companies are seeing productivity and efficiency gains.[4] While this technological revolution may be driven by industries that are keen to invest in new technologies to solidify their place in the market, the gains can and will also be passed onto more traditional industries as discussed above.

One of the Government’s flagship policy areas is the Levelling Up agenda. This agenda aims to ensure that everyone in the UK can flourish by ending the extensive geographic inequality between different local areas. The objective of Levelling Up policy is to increase productivity, employment, pay, and living standards by growing the private sector, especially in areas that are currently underperforming.

The Government’s ambitions were set out in the February 2022 Levelling Up White Paper, which outlines 12 Levelling Up missions intended to provide clarity and consistency on policy objectives across government, with measurable outcomes by 2030. These missions cover a wide range of areas, including living standards, innovation, skills, and pride in place. Alongside each of these missions the Government published a series of provisional metrics against which progress on each mission is to be monitored. These metrics, particularly the metrics for mission 1 (living standards) provide a framework for understanding how growth in the digital tech sector can contribute to the Levelling Up agenda. These metrics are divided into headline metrics which will be the primary indicators used to measure progress and supporting metrics designed to supplement these primary indicators.

The regional data analysis suggests that there is significant opportunity for growth in the digital tech sector to contribute towards these policy objectives, especially GVA (productivity), median weekly pay and the proportion of skilled employment. As was highlighted in section 3.2 GVA per hour worked in the digital sector is considerably higher in the digital sector than the region overall (£42 versus £31). Not only this, but there is evidence from other regions that productivity can grow still further. Further growth in the size of the sector can contribute to raising productivity across the North East LEP.

In terms of median weekly pay the digital sector has the highest median gross weekly wage of any sector in the North East region. Not only this, but most digital occupations also have average renumeration above the North East average. Further growth in the sector therefore can also contribute to increasing pay in the North East as a whole. It should be noted however, the relatively large proportion of individuals employed as IT user technicians in the North East region, which have a low income compared to most digital occupations, may limit the potential of the sector on this metric.

Not only are digital tech occupations generally well paid, but all the occupations classed as digital occupations by the DCMS are within SOC codes 1-3,5 and therefore contribute to the Levelling Up metric ‘Proportion of employed people in skilled employment’. As was noted in the regional data analysis there are already 47,600 individuals employed in digital tech occupations in the North East region. Increasing this number will further increase the rate of skilled employment. It will also contribute to the North East LEPs own target of creating more and better jobs in the North East.

Internationalisation

A further element of the UK government’s policy agenda is to increase the value of the UK’s exports. Made in the UK, Sold to the World was released in November 2021 and is a refresh of the UK’s previous 2018 trade strategy. The ambition of the strategy is to reach £1 trillion exports annually before the current projections which suggest that milestone will be reached in the mid-2030s.

The strategy is to be supported through a 12-point action plan. A key aspect of this plan includes the opening of new markets to UK exports through new trade deals, with the ambition to have these cover 80% of UK trade by the end of 2022. This includes trade deals that have been reached in principle with Australia and New Zealand and the ambition to ascend to the CPTPP, one of the largest free trade areas in the world covering Asia pacific and the Americas. The Government also announced the beginning of free trade negotiations with India in January 2022 with an aim to conclude an agreement by the end of the year. These future agreements are focussed on the Asia-Pacific region as the Government believes future world growth will be driven by markets in this area.

The wider North East region has a significant opportunity to capitalise on this strategy, as the North East already has a high exports per head compared to the rest of England. Specific aspects of government policy are also likely to create opportunities for the North East region. For instance, the Government has opened a second DIT headquarters in Darlington, providing close proximity to the DIT for regional exporters. The opportunities provided by this infrastructure on the North East’s LEP’s doorstep have the potential to significantly increase the exporting capability of the North East LEP.

The North East LEP is also actively working with partners across the region to increase North East exports, having published a new trade and exports report in June 2021. This report highlighted opportunities to build on existing high levels of exports, the trend of increasing global service exports and the growing digital transformation of manufacturing.

The direct contribution of the digital tech sector to regional exports is likely to be relatively modest, for as was highlighted earlier the sector only contributes around 5% of North East service exports. Exports per person employed in the sector, while stronger in the North East region than other Northern regions, is still much lower than in the South and London. There is room for improvement, but the sector is unlikely to itself drive a significant proportion of North East exports directly.

Net Zero

Net Zero is a key part of the UK government’s agenda having brought forward legislation in 2019 committing to Net Zero by 2050. In 2021 the UK also held the presidency to the 26th Conference of the Parties (COP26) in Glasgow and released its Net Zero strategy ‘Build Back Greener’. This latter document outlines how the Government intends to fulfil its commitment to reaching Net Zero.

The North East region is in a strong position relative to its regional comparators in the drive to Net Zero, although there is still considerable further progress required. Excluding externalities emissions from the North East LEP have already halved between 2005 and 2019. This leaves annual emissions of 7,817 kt of CO2 for the North East LEP region (2% of the UK total), with the North East LEP also having lower per-capita emissions than England excluding London.

However, there is still significant progress to be made, progress which is not possible without the successful adoption of digital and related technologies. For instance, the International Energy Agency has highlighted digital technologies have an important role to play in developing international capacity for energy efficiency.

Digital technologies offer the potential to use the ever-greater volume of data collected on energy use and production to find ways to reduce overall energy consumption. As was discussed in the literature review, the adoption of digital technologies is also crucial to the development of industry 4.0, which itself is critical to the development of Net Zero technologies such as electric vehicles. Without the effective adoption of digital technology throughout the manufacturing supply chain there will not be enough effective capacity to enable a wider transition towards a Net Zero Economy.

It should also be noted however, that some aspects of the operations in the digital sector are very energy intensive (particularly data centres which accounted for 1% of global electricity use in 2018)[1]. Efficiencies in tech has helped mitigate the environmental impact of digital sector growth so far. Still, the digital transformation must occur in conjunction with the decarbonisation of the energy grid to prevent digital growth from negatively impacting on the environment.

The fact that many tech workers can work from home also has an ambiguous impact on carbon emissions per worker. Those who work from home do generally create fewer emissions from travelling. However, as domestic heating standards are generally poorer than those in offices during the winter working from home can lead to increased carbon emissions[2]. Digital tech can enable new sustainable working practices, but this must be supported by wider progress on decarbonisation and energy efficiency.

^Energy innovation, How Much Energy Do Data Centers Really Use? (2020)

^BBC, Why working from home might be less sustainable (2020)

Innovation

Underpinning the Government’s ambitions with respect to building back better, Net Zero and internationalisation is their innovation strategy. This strategy highlights successful innovation in the private sector is an essential part of the UK’s future prosperity and therefore essential to achieving the UK’s other objectives. The innovation strategy was released in July 2021 and states that the Government’s objective is to make the UK a global hub for innovation by 2035. To achieve this the strategy outlines a series of key actions, grouped into four pillars, unleashing businesses, people, institutions & places, and missions & technologies.

Innovation is almost by definition very difficult to measure. Yet as was highlighted in the regional data analysis, there is experimental evidence that the tech sector is very innovative compared to the rest of the North East LEPs economy. 30% of digital tech firms in the North East LEP area were classed as highly innovative by the Data City platform. Growth in the tech sector therefore can help contribute toward the Government’s innovation agenda.

Technology is also linked to innovation in a more fundamental way because the adoption of new technologies is itself often a driver of innovation. It is through the adoption of new technologies that firms can identify new opportunities for product or process development, and therefore technology plays a key enabling role facilitating innovation across the wider economy.

Supporting wellbeing in old age

A further policy area where digital technologies are well placed to make a significant contribution is supporting wellbeing on old age. As has been highlighted by the NHS the UK has an ageing population and the challenges in supporting this ageing population are likely to increase over the medium term. More than one in five residents of England are already over the age of 60, and the number of individuals aged over the age of 60 is expected to increase to 18.5 million by 2025. Not only this but advances in health care have helped increase life expectancy without necessarily increasing healthy life expectancy. 75% of 75-year-olds in the UK already have more than one long term condition.

Digital technology can contribute towards supporting wellbeing in old age through the development of new kinds of assistive technology. For instance, AgeUK have highlighted how advanced information technology has made possible new forms of telecare, telehealth and robotics that can support the elderly to stay in their own homes longer. This can potentially contribute towards supporting wellbeing in old age, provided the development of such technology is properly integrated with the existing care system, for these technologies are unlikely to be a full substitute for human centred care.

The North East LEP area is particularly well positioned to contribute to the development of digital assistive technology due to the fact it hosts the national innovation centre for ageing in Newcastle. This centre supports the translation of research into practical solutions, and therefore is ideally placed to help technological developments have a meaningful impact on human centred wellbeing.

Existing regional technology assets

Infrastructure

The technology sector in the North East LEP can take advantage of the 21 sites across the North East Enterprise Zone. These sites provide either business rates discounts or enhanced capital allowances which can allow firms in the North East LEP to gain a competitive advantage. The sites were strategically selected to build on existing strengths across the North East LEP’s economy, including the technology sector. They are also dispersed widely across the North East LEP areas allowing businesses across the whole region to benefit from the available opportunities.

The Newcastle helix is a 24-arce testbed and collaborative eco-system for public and private sector bodies. Providing state of the art office space and proximity to other innovative firms and organisations, including the national innovation centre for data, the Helix creates the conditions for a thriving local tech eco-system.

One of the largest business parks in the UK, the Cobalt business park is located in North Tyneside and currently hosts a range of technology companies including EE, IBM and SAGE group. The site also contains Europe’s biggest purpose-built data centre.

Is a unique science park in Sedgefield home to over 40 companies employing over 600 people. It is the only UK science park with two national catapult centres, and provides a mix of infrastructure, collaborative opportunities and support for science, engineering and technology companies.

Part of the Digital Catapult North East Tees Valley network, PROTO Gateshead provides animators, filmmakers and games developers access to 3D scanning, motion capture and sound recording. It is the first digital production facility of its kind in Europe.

The North East LEP has many incubators and workspaces that can be used by firms in the digital tech sector, including Tuspark, Entrepreneurial Spark, Business and Innovation Centre (BIC) Sunderland, Durham City Incubator, PROTO, Sunderland University Enterprise Zone Digital Incubator, Hoults Yard, Norther Design Centre, Evolve Centre, Toffee Factory, Newcastle Helix.

Innovation and business support

Sunderland Software City (SSC) aim to address the changing needs of the tech sector through a range of innovation, digital skills and business support programmes. Their business support programme provides 12 hours of fully funded specialist support to digital and non-digital business across the North East LEP area. Sunderland software city is also responsible for the delivery of the Digital Catapult North East Tees Valley.

Sunderland software city’s innovation support activities are delivered as part of the Digital catapult North East Tees Valley, the North East part of the national digital catapult network. The focus of this work is helping to educated traditionally non-digital businesses about the potential applications of advanced digital technologies. To do so the catapult delivers a wide range of services including one-to-ones, innovation workshops, hackathons and horizon-scanning services.

The devolved authority for the North of Tyne area (Northumberland, Newcastle and North Tyneside) has a strong commitment to supporting digital growth and innovation. Through their digital growth and innovation programme the authority has invested £10 million to support the growth of the digital sector. This programme includes six sub programmes, which support digital adoption, inward investment, cluster development and the digital business pipeline in the North of Tyne area.

Located in the Newcastle Helix, the national innovation centre for data helps organisations large and small generate insight from data, including organisations in the Tech sector. The centre receives funding from the North of Tyne combined authority as part of the digital growth and innovation programme.

The Made Smarter programme supports businesses to get to market faster, cut costs and reduce downtime. It does so by helping businesses invest in digital tools, innovations and skills. Support through the Made Smarter programme in the North East LEP is available via the North East Growth Hub.

Is a further site in the CPI that accelerates the commercialisation of printed and flexible electronics. By providing an environment where companies can test and develop concepts the centre supports innovators through the challenges of scaling products and process.

The Innovation Supernetwork aims to help North East businesses bring innovative products and services to market. They do this by providing bespoke innovation support to small and medium sized enterprises in the North East LEP area, as well as increasing connectivity and sharing best practice.

Is an independent digital support network dedicated to promoting the North East of England's Digital and Information Technology sector.

Is a £4m initiative (funded by the European Regional Development Fund) that aims to help SMEs in County Durham to maximise their growth potential and sustainability through digital technology.

Is an open community for the digital creative industries working to strengthen the North East’s tech sector and promote it to the rest of the UK.

Is an industry led group with the core mission to ‘Grow the North East Tech Economy’ through collaboration, innovation, skills. They act as a voice for the region promoting it as a centre of tech development both regionally and nationally.

Is a nationwide growth platform (with local presence) focussing on building the tech sector in the UK.

Are an independent, cross-sector group for digital influence, leadership and innovation. They work to help businesses across all sectors solve their challenges through the innovation use of technology.

A centre of excellence for digital construction and transformation that helps businesses apply building information modelling (BIM), smart processes and digital technologies to accelerate their output.

Enabling sectors

The North East LEP is home to four universities, Newcastle, Northumberland, Sunderland, and Durham. These universities are a critical source of skills for the region, including the tech sector. In 2020/21 there were 5,165 students enrolled in computing degrees in these four universities.

There are nine further education colleges in the North East LEP area, providing critical technical education and further learning opportunities. These colleges are brought together through the North East LEP area College Hub which brokers strategic employer partnerships with further education institutions.

The North East LEP has a substantial financial, professional and business services sector. This includes the headquarters of established brands such Virgin Money and Newcastle Building Society, and new and innovative companies such as Atom Bank, World Pay, True Potential, Wire Card and Scott Logic. The major presence of this sector provides technology firms in the region with access to financial and business support services that are key for supporting growth.

Methodology

Data analysis

Technology has often been referred to as the application of scientific knowledge to practical aims and objectives. Because this definition is inherently innovative, it means that defining and measuring the digital tech sector is especially challenging, not least because technology can be applied in many sectors.

To mitigate this uncertainty, we have collected data from a wide variety of sources, both quantitative and qualitative, and triangulated the findings from an array of perspectives. In terms of quantitative analysis there were two main stages. The first was a regional data analysis using a broad definition of the sector to develop a high-level perspective on the sector in the North East. The second stage was a fine-grained analysis of sector level data focusing on specific subsectors and their presence in the North East LEP. The results from these two stages complement each other by providing both a top-down and bottom-up view on the regional digital tech ecosystem.

For the regional data analysis, we used the Department of Digital Culture Media and Sport’s (DCMS) definition of the digital sector, which is widely used by the Government and other sector bodies. This definition has two parts, covering:

The Digital tech sector – This is used to measure identify firms who operate in the sector, but employees in these firms are not necessarily working in digital tech roles

Digital tech occupations – This is used to measure those who work in roles related to digital tech but do not necessarily work in the sector itself

The definitions use the standard industrial classification codes (SIC codes) and standard occupational codes (SOC codes), with different levels of precision for different datasets. The full SIC and SOC definitions are available on request.

We recognise however, that these definitions have limitations. Therefore, we used the innovative Data City platform to provide firm level sector data too. The Data City classifies firms according to their website text rather than their SIC code to provide an alternative typology (the methodology is discussed in greater detail below). This complements the findings from the regional data analysis with firm level intelligence on the specific sector strengths in the North East.

Finally, to ensure that we did not overlook existing insight, we also conducted a literature review of existing research reports and policy papers, consolidating the findings in the literature review section of this evidence base.

It should be noted that this evidence base does not cover the broader concept of digital skills beyond those who work in digital tech occupations, as it has been designed for the purposes of developing a sector focused tech strategy.

Data City methodology

There are limitations to the publicly available data sources when analysing emerging and fast paced sectors such as digital tech. To help mitigate some of these limitations we have supplemented our analysis with data from the Data City platform. This platform links companies house data to companies’ websites and uses the website text and machine learning to classify firms into Real Time Industrial Classification Codes.

Gathering data

The Data City web-scrapes activities off company websites...

Linking data

...and links this to Companies House data...

New taxonomies

...to create a taxonomy of UK companies beyond SIC codes.

There are two key advantages to the taxonomy of firms provided by the Data City. The first is that by using a company’s own description and narrative the platform can provide business counts for fast emerging sectors that are not captured well (or perhaps at all) by SIC codes. Firms can also be classified in more than one sector in the Data City taxonomy, unlike SIC codes which are a 1 to 1 classification system. This allows the user to understand the interdependencies between sectors.

In addition, the platform also scrapes location data from firm’s websites. This allows the platform to identify companies that have a branch or office in the North East LEP even if they are located elsewhere. All the analysis in the sectoral analysis sections uses these additional locations. We have also used this data to understand the extent that different sectors have a branch economy in the North East LEP area.

Based on the North East LEP’s existing knowledge of the sector and the literature review nine sub-sectors were selected to explore their regional presence in the North East.

Further evidence

Our economy 2022

Read our annual state of the region report on the North East's economy